Profit does not pay payroll; cash does

A service company can be profitable on paper and still run out of money, because profit and cash are not the same thing. You do the work, then invoice, then wait, while payroll leaves on a fixed schedule regardless of when clients pay. Cash flow management is the practice of watching that gap closely enough to act before it becomes a crisis: forecast a few months ahead, hold a buffer, and pull the timing levers you control.

Use this if revenue looks healthy but cash still feels unpredictable, or if you only check the bank balance when a big payment is late.

Why profitable service companies still run out of cash

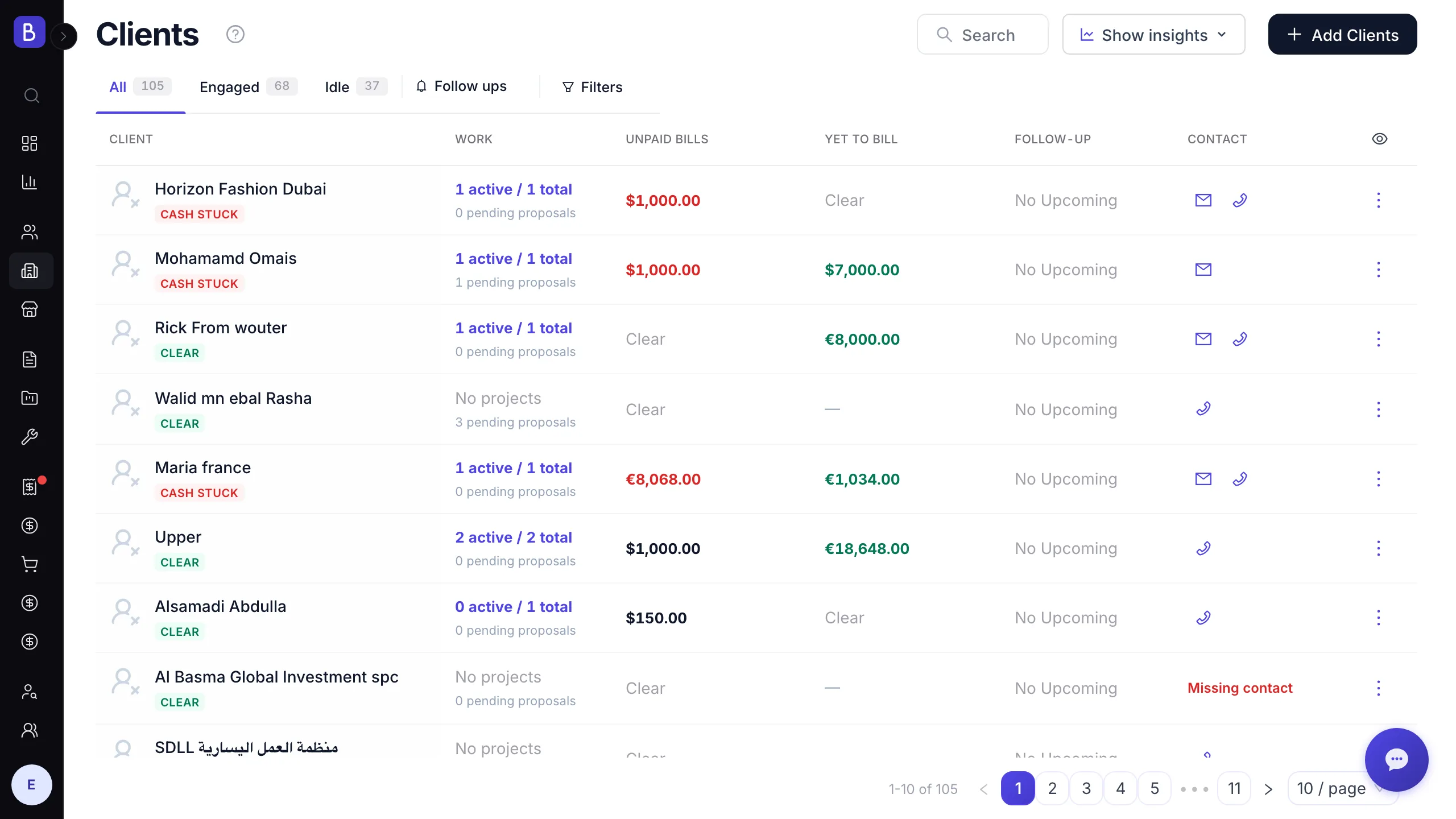

Product businesses usually collect at or before delivery. Service businesses do the opposite: you deliver first, invoice second, and collect third. Your largest cost, payroll, hits on the 1st and the 15th no matter what your clients are doing. Finish a project in January, invoice at month end, offer Net 30 terms, and a client who pays a couple of weeks late has you waiting forty-five days between delivering value and seeing the cash. In that window you have run payroll twice.

That gap, not a lack of clients or bad pricing, is what strains otherwise healthy firms. It gets worse in the feast-or-famine cycle: you win a wave of work, everyone goes heads-down to deliver it, nobody sells during delivery, and the pipeline is empty when the projects wrap. Costs stay flat while revenue dips, and the "best quarter ever, then worst quarter ever" pattern is born. Understanding that cash lags revenue is the whole starting point.

How much cash buffer do you need

A cash buffer is real money in a separate account that you do not touch unless you need it to cover a gap. As a rule of thumb, aim for two to three months of fixed costs (payroll, rent, software, insurance) once your business is established. Newer firms with less predictable revenue should aim for the higher end, because their income swings more. Two things push your target higher: heavy client concentration (if one client is a large share of revenue, one late payment hurts more) and long project cycles (the more time between billing events, the deeper the cash trough you have to bridge).

The number can feel impossible when you first calculate it, so build it gradually rather than all at once. A practical method is to move a fixed percentage of every incoming payment, say ten percent of revenue and not of profit, into the buffer account the moment it arrives. It will feel tight for a while. The first time a large client pays two weeks late and you do not have to scramble, it pays for itself. A line of credit is a useful backup, but it is a backup, not a strategy; you are paying interest to cover a gap that planning could have prevented.

Invoice timing is your fastest cash lever

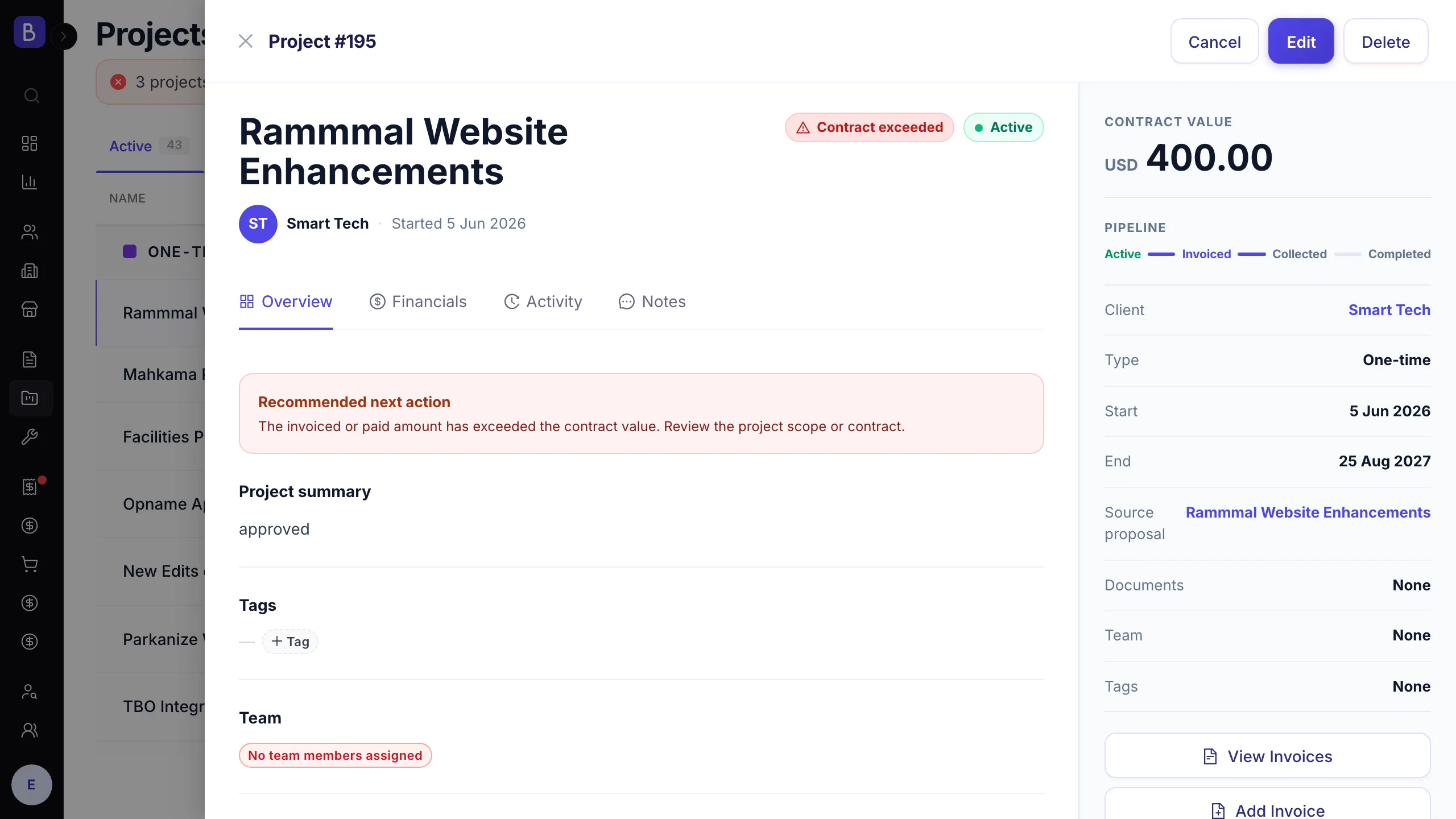

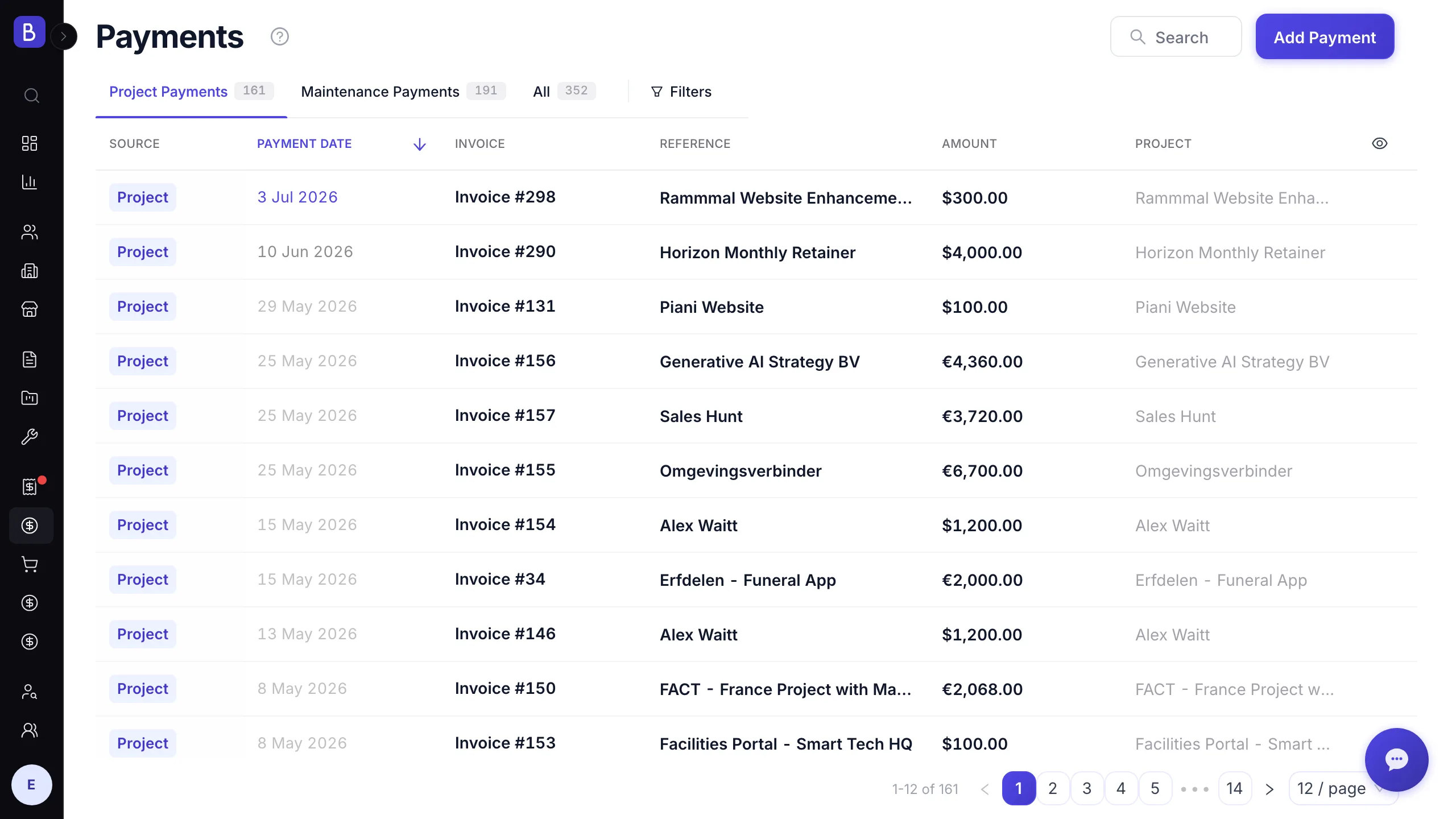

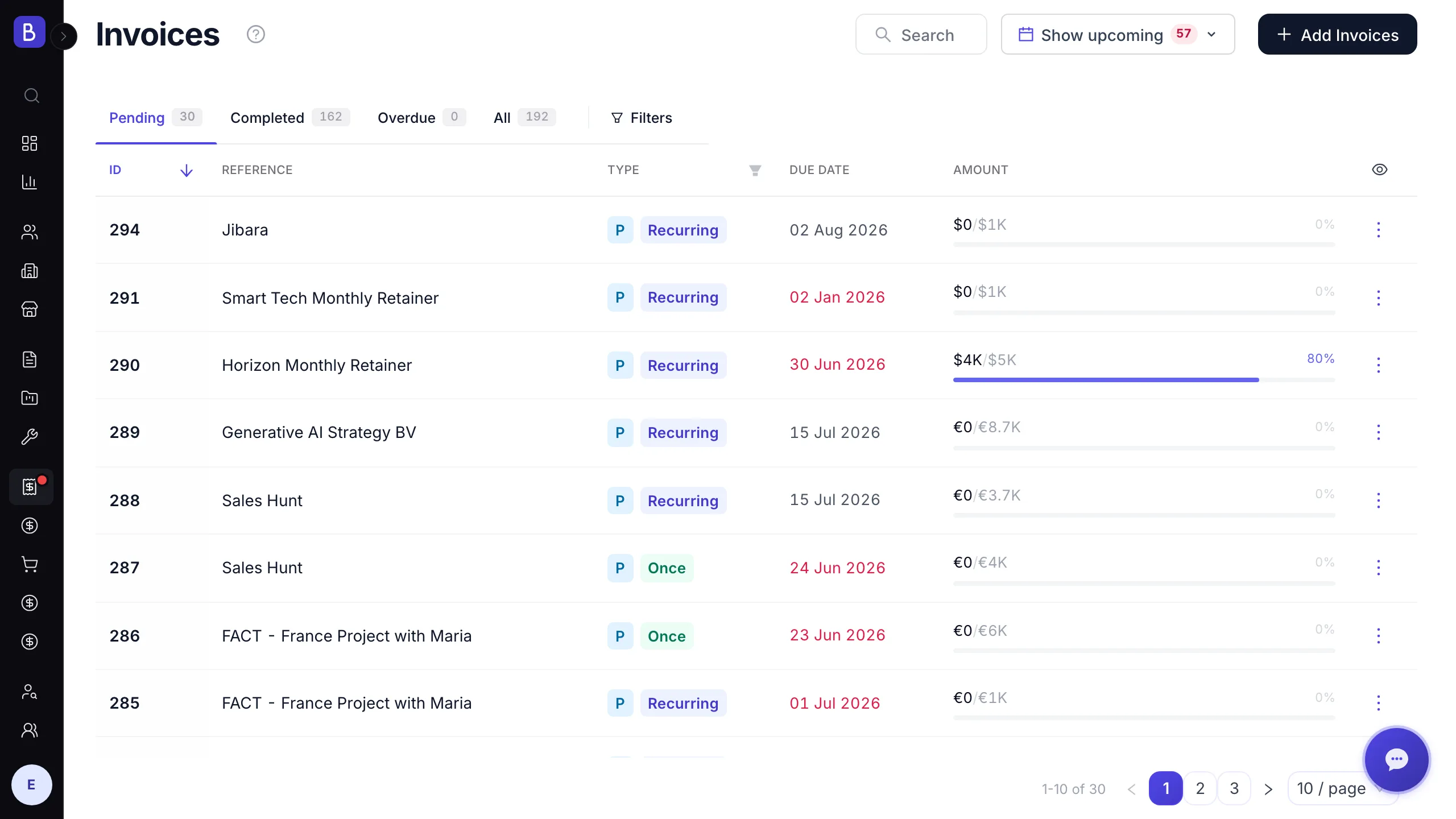

You cannot always make clients pay faster, but you fully control when the invoice goes out and how the terms are set. The single highest-impact change is to invoice the same day a milestone is approved, while the value is fresh, rather than batching everything to month end. Every day between finishing work and sending the bill is an interest-free loan to your client. The tactics that get those invoices paid on time, shorter terms, a follow-up cadence, and milestone billing, are covered in detail in our guide on getting clients to pay on time.

Beyond timing, a few structural levers smooth the flow:

- Require a deposit before reserving delivery capacity, so a canceled project does not leave you eating the first two weeks of cost.

- Bill larger projects across milestones instead of one big invoice at the end, which is always the hardest to collect.

- Turn repeat work into recurring agreements so a known amount arrives on a known date.

- Stagger project starts by a week or two so deliverables, and the invoices that follow them, do not all land in the same window.

Watch your runway, not just your revenue

Revenue is the work you earned. Cash on hand and runway tell you how long you can operate if income paused. Track your receivables by age so the money that needs attention is obvious: accounts receivable aging groups every unpaid invoice into current and increasingly overdue buckets, so a slow-paying client cannot quietly become a cash problem. Alongside it, days sales outstanding tracks how long collection takes on average, so you can tell whether your process is improving or drifting.

If those two measures are climbing, fix your billing and follow-up before you chase new sales. A live view of cash on hand, money in and money out, outstanding invoices, and runway, like the one in analytics that shows how many months of runway you have and roughly what you are burning each month, turns "I think we are fine" into a number you can act on.

The weekly cash review

The habit that separates owners who sleep at night from those who do not is a short, regular cash review. Once a week, spend fifteen minutes updating a simple thirteen-week forecast: starting balance, expected client payments by week, payroll and contractor costs, rent, software, taxes, and the running balance at the end of each week. Thirteen weeks is long enough to see trouble coming and short enough to stay accurate.

Then look at one thing: the lowest projected balance in the next three months. If that low point is uncomfortable, you now have weeks to react instead of days. You can accelerate an invoice, follow up on a late payment, delay a non-essential purchase, or draw on your credit line before it becomes an emergency. The tool does not matter; the practice does. Forecasting your cash weekly and looking a quarter ahead is what stops every month from feeling like a survival exercise.